CRE Lesson #3: False Precision: My Back of the Napkin Tricks are Better than your Pro Forma

Three easy metrics to improve your acquisitions funnel

"The only thing I know about every pro forma I have ever built is that it's been wrong." - Me

Acquisition people like to brag about our gut; we claim an innate ability to sniff out deals.

But what we really excel at is sifting through a bunch of junk to find the deals that are "maybe" good. That's how you find the great ones.

If you sit down with most big money real estate private equity players however, you’ll inevitably end up hearing about their "model." Which is usually a multi-tab excel monstrosity with a crowded page of inputs that drive a complex machinery of cash flow projections that spits out expected returns based on unknowable things like future rent growth and exit cap rates seven years from now.

These big complex models impresses their investors who never bother to visit an actual property, then wonder why they were buying at the top of the market.

It’s not that financial analysis is bad, but too much of it gives the impression that you know things you don’t actually know. It can trick you into thinking that you can “model away risk,” which is absurd, yet an idea that has surprising traction in the ivory towers of certain coastal financial hubs (not to mention within certain highfalutin universities, but that is another post for another day).

So how do you evaluate a potential deal without a financial model?

Real estate people answer this question with a bunch of terms designed to show their peers that they know the market. The better your lingo, the more capital you have behind you. Obviously.

“Simplicity is the ultimate sophistication.” - Leonardo da Vinci.

Enter “back of the napkin” analysis that real estate pros for generations have used to value properties, well before Excel revolutionized the business of modeling away risk.

And the big bad secret that Wall Street money doesn’t like to hear is that they work. Really well.

Here are my three favorite shorthand valuation methods to help you screen more deals and focus your energy on the diamonds in the proverbial rough.

But first, a few caveats:

1) These metrics work in the markets in which I operate, so they may need to be modified for whichever sandbox you happen to be playing in.

2) Using these metrics without the market knowledge to know their limitations is another word for lazy.

3) Back of the napkin tricks are no substitute for rigorous financial analysis of a prospective deal which, despite its flaws, is essential if you are investing other peoples' money.

MY BACK OF THE NAPKIN VALUATION TRICKS (also known as “AJ’s secrets to real estate”)

1) Garden Style, Institutional Multifamily

They key to a good back of the napkin is that it’s so simple you can do the math in your head. The simpler, the better.

Imagine that an offering memo for a garden style multifamily deal in the American heartland lands on your desk, 70 full-color pages of fluff telling the story of the unmatched potential and robust job growth of some suburb you've never heard of.

How do you decide whether its worth your time? Simple math.

Monthly rent x 100 = price per door

That's it, that's the math.

Why? Here goes:

I mean that’s pretty close. And with math my 9-year old can do in her head.

For markets that trade a bit tighter than a 6-cap, push up the price per door you're willing to pay, and vis versa for markets that trade wider.

If a deal passes that screen, move onto the next step of underwriting. If it doesn’t, tag and release.

2) Office Repositioning

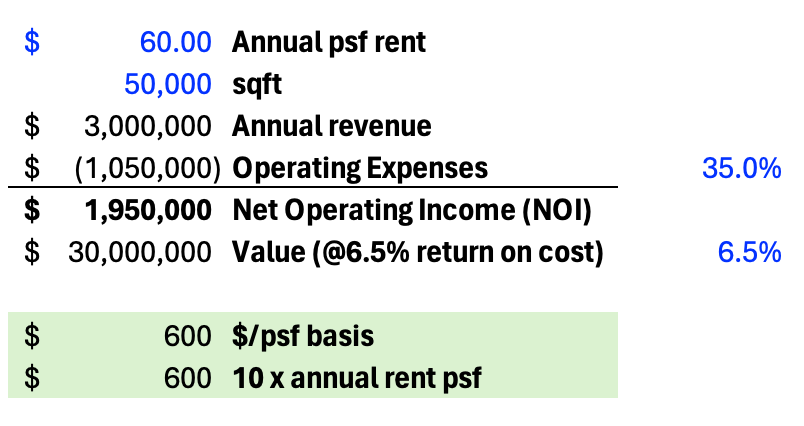

The back of the napkin calculation for an office deal is just as simple, and is even more precise.

Annual market rent x 10 = Target basis for a 6.5% ROC

That means you could pay $500psf with a $100psf capex/TI budget, or you could buy at $400psf and plow in $200psf. Either way, you'll end up at the same ROC, or return on cost.

Don’t worry about your capital structure, deal fees, carrying costs until you get into the real analysis - which you shouldn’t bother with unless this back of the napkin checks green.

3) 7-year Value-Add Project

The last one is a bit more nuanced, even though the math is just as easy.

Sell for twice where you buy

Let’s break down why this works, and then how to apply it, because if you layer this one top of the other two, 80% of your financial analysis for a deal is already done.

To raise money in your average value add syndication, LPs want to see between a 12-15% IRR, a 2x equity multiple, and a hold period of not longer than seven years. Once you add the benefits of leverage (which exist even in this environment) to the math above, then add positive operating cash flow and back out deal fees and promote, you end up right in that sweet spot of a 12-15% levered return (if none of that made sense, don’t worry and trust da Vinci.

No matter how many times I tell people this and they don’t believe me, we run the numbers, scrub the pro forma and end up where I started - sell for twice where you buy.

Obviously, for heavy value add deals you’ll want to lean towards selling at twice your Total Project Cost, and for cash flow heavy deals you can probably sell for a bit less than a double since that positive cash flow is accrues to the deal. And because investors love to focus on IRR, the earlier cash flow from operating profits will push up the IRR more than the same amount of cash at sale (time value of money).

The best way to apply this third rule is using basis, rather than price. Depending on the market, you’ll want to use either price per foot or price per door, and look forward at an exit price of twice what you are paying.

So if a property is listed at $300psf and you can see a realistic world where it sells for $600psf seven years from now, it's worth taking the next step. If that seems like a pipe dream, best to move on.

Which brings up the trickiest part of applying this rule: Projecting valuations in the future is hard by definition, and it's easy to get anchored by today's prices.

“There is no way an apartment building in the Mission will sell for $600psf seven years from now," is a reasonable thing to say if market prices are $300psf. This is exactly what I was saying back in 2011, when lo and behold, in 2018 that is exactly what they were selling for.

SO …. WHAT?

So, why does this even matter? Why bother estimating the value of a property when with a bit more work you can actually figure it out (to the extent anyone can figure out the true value of a property)?

The reason is pretty simple: it's my job.

My job is to find the one deal among the hundred that is worth doing. And if I fully underwrote every deal that came across my desk, I’d never find the great ones.

I'd never have time to talk to brokers about what you don't read about in the press, never have time to talk to other operators to find out what you don't hear from brokers, never be out in the field crawling around buildings looking for hidden potential, and I'd never be out walking the streets to find the next up and coming neighborhood.

I'd never have time to dive deeply into the (maybe) good ones if I didn't know how to throw out the bad ones.

A lot of people mistake acquisitions for being able to "spot the deal." And sure, there is some of that in what we do.

But its more likely that I just choose to forget the deals where my spidey sense went off, and it turned out to be a dud.

Monthly rent x 100 = price per door. What a beautiful work of art!

Based upon this formula one could back in stabilized YOC to see if it's 200 BP above the cost of debt.

Great info!

Thanks