Five Things You Need to Know: REIT Pricing Predicts A Market Bottom, Fed Tightrope Narrows

CRE industry grasps for optimism amid worsening delinquency data

During a stint at Minyanville, a financial news and education media company, I was fortunate to work under the tutelage of a talented editor named Kevin Depew. Depew is now the deputy chief economist at consulting firm RSM, and wrote prolifically during the Great Financial Crisis, brilliantly capturing the mood of America during that trying time. His "Five Things You Need to Know" was required reading every week, and covered topics from high finance to macroeconomics to social trends. This series is an homage to "Pep," who once quipped "I majored in philosophy, but since none of the big philosophy firms were hiring, I went into finance."

1) CRE Investors Talk Themselves into a Bottom

After a forgettable 2023, the commercial real estate world is grasping for optimism. And behind the scenes, investors are accumulating piles of cash, eyeing depressed valuations and mounting distress across property sectors.

According to Bisnow, Caryle co-founder David Rubenstein is raising $400 million to target multifamily and industrial properties, in the latest announcement of investors raising opportunistic funds.

These efforts are being repeated across the industry, with SLG Green (NYSE: SLG), Ares Management (NYSE: ARES), BlackRock and others looking to capitalize on distressed opportunities.

These opportunistic buyers are betting on an imminent bottoming of prices, rooted partly in the expectation that the Federal Reserve is on the brink of an easing cycle. But the assumptions underpinning those hopes are beginning to slip, as even Federal Reserve Chairman Jerome Powell said this week that rate cuts would come later in the year than investor forecasts.

Meanwhile, economic data remain resilient, despite recent job cuts and evidence that stretched consumers are running out of steam. Inflation is down substantially from this time last year, but geopolitical risk and other input-related flareups make the Fed's dual mandate of controlling inflation and maximizing employment a tricky balancing act - especially in an election year.

With delinquencies continuing to rise, according to real estate data provider Trepp, investors’ best friend in the coming months may be patience.

2) Multifamily Quietly Corrects

Despite strong long-term fundamentals, the once-mighty multifamily sector is quietly falling apart. According to analysis and data provider Green Street, multifamily pricing has been the second worst performing sector in CRE over the past 12 months, with prices down 12%. Only office has fared worse, with prices down 25%.

And since its peak in 2022, multifamily prices are now down 30%.

Wall Street agrees, taking down apartment owners Equity Residential (NYSE: EQR) and Avalon Bay (NYSE: AVB) each around 30% from their peaks in 2022.

Publicly traded REITs are good leading indicators of private deal pricing, since their immediate liquidity gives investors a chance to react to market data in real time. And since actual property sales take months and sometimes years to complete, REITs valuations often bottom out well before the corresponding values of their actual portfolios.

The question is whether REIT pricing has come down far enough, and some industry participants are saying the quiet part out loud: Distress is just getting started.

At a recent housing conference, I milled through the crowd of blazers and peddle pushers and listened to mostly optimistic deal chatter. But during an actual discussion, a Texas multifamily investor leaned over to me and said quietly, "There is a ton of distress out there, it's coming. And all these guys know it."

If the Fed doesn't come through on hopes of lowering borrowings costs sooner rather than later, multifamily owners with maturing debt and sagging rent rolls may find themselves even further upside down than they already are.

3) Office Tug-O-War Heats Up

The option to work remotely, at least part of the time, has now become ubiquitous across American industry.

But as the labor market tightens and companies tire of managing hybrid work arrangements, the tug-o-war between capital and labor is intensifying.

The Wall Street Journal reports that UPS (NYSE: UPS), after announcing 12,000 layoffs earlier in the week, is following JP Morgan (NYSE: JPM) and Boeing (NYSE: BA) in mandating five days a week in the office for some segments of their employees.

This battle over where to work will determine the fate of the beleaguered office sector. By most estimates, the recovery of urban office markets will be measured in decades rather than years, as organic demand growth chips away at giant swaths of unused space being.

But if bosses are able to gain the upper hand and push workers back to the office, it could be a badly-needed respite for owners of downtown office properties.

In fact, I contend that the biggest potential Black Swan in real estate is the collapse of the hybrid work experiment. Those office properties trading at prices not seen since the 1990s may be cheaper than we think.

4) Fed Tightrope Narrows as Banking Crisis Flares Up

Fed Chairman Powell's unenviably task of navigating competing economic motivations during an election year didn't get any easier this week.

New York Community Bancorp (NYSE: NYCB), which scooped up assets on the cheap from failed lender Signature Bank last year, warned of mounting losses in its real estate portfolio and cut its dividend. Shares were down 40% on the week and regional banking stocks tumbled, as investors were reminded that someone, at some point, will have to plug the $1 trillion (with a T) hole in balance sheets stemming from plunging commercial property values.

Lenders under pressure from unrealized losses would benefit from lower rates, but the Fed may be hesitant to extend its record of being undefeated at predicting recessions.

The beginning of every recession since the 1950s has been marked by the Fed lowering interest rates.

And regardless of whether this is correlation or causation, Powell is aware that while markets may cheer his more dovish stance on on rates, actual rate cuts send the message that all is not well on Main Street.

5) Where is Everybody Going?

Back in college I had this burning question: where is everybody going?

You pass countless people going around the world, all going somewhere, and I wanted to know where. Were they going home? To work? Shopping? To visit a lover? Where were they all going?

I imagined a study where I would follow people around until they got wherever they were going to collect enough data to finally answer that elemental question. A bit stalky and it never happened, but the question remains.

Now online real estate brokerage Redfin is doing their own spin on my decades-old musing, using their property search activity to assess migration in and out of American cities.

In other words, to find out where people are going.

At first glance the data seem to confirm some widely held views about which cities are hemorrhaging residents and which are hoovering in new arrivals. But upon further inspection, the data are not what they purport to be.

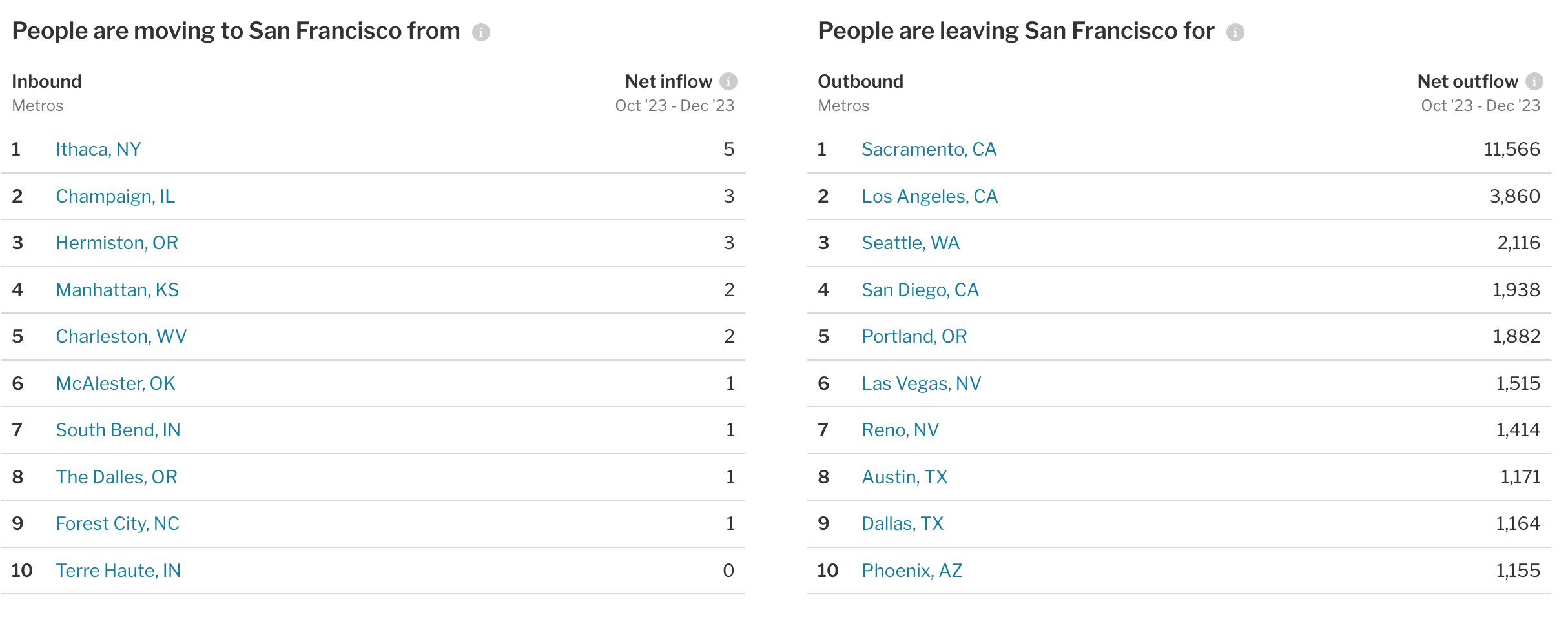

According to the Redfin, the graphic below would have us believe that by a nearly unanimous ratio, people just cannot get out of San Francisco fast enough and essentially no one wants to move there. Which fits the popular narrative, that San Francisco is a crumbling cesspool.

Yet, according to a recent study by the California Finance Department, San Francisco notched its first year-over-year growth in population since the pandemic.

So how could Redfin's data be so wrong? Let me count the ways.

First, the fine print."Net inflow is the number of Redfin.com home searchers looking to move into a metro area, minus the number of searchers looking to leave."

So when Redfin says “People are moving to San Francisco from,” they don’t actually mean that. The column labeled "Net Inflow" is not actually inflows of people, but searches.

Second, that search data is highly skewed, since it reflects home searchers, not rental searches. Rare is the transplant to San Francisco, or any high priced urban area, who starts off as a home buyer. So by ignoring those searching for rentals, Redfin can hardly call their net searching number "inflows," even if one expands the definition to include aspiring newcomers.

Third, searching is not moving. San Francisco, while having quietly become among the most affordable big cities in the country, remains more expensive than most other parts of California.

So it's natural for curious San Franciscans to wonder where they might be able to relocate and keep more of their salary. Hence Sacramento being the top "search" destination, followed by nearby western metro areas.

Lastly, Redfin searchers may just as easily be poking around for investment property as a new home. But since intent isn’t shared, we can't know how many of these Inflows and Outflows are actually a potential buyer looking for an investment opportunity.

The Redfin data is clearly displayed, with a nifty map (that could benefit from some arrows), but the information is so deeply disingenuous that one has to wonder if the company is seeking to paint an accurate picture of demographic trends, or is merely hoping that snazzy graphics will keep home searchers on their site long enough to book a commission.