Three Commercial Real Estate Stories You Didn't Read This Week (but Should Have) - Dec 8, 2023

Plus my take, plus ChatGPT's take

Every week I scrounge the commercial real estate (“CRE”) rags and the occasional mainstream source for the most important, or perhaps soon-to-be-important, stories that may have slipped through the cracks. I summarize the piece, explain the broader implication and then give our friends at OpenAI a shot by asking ChatGPT a question about the story.

MY TAKE

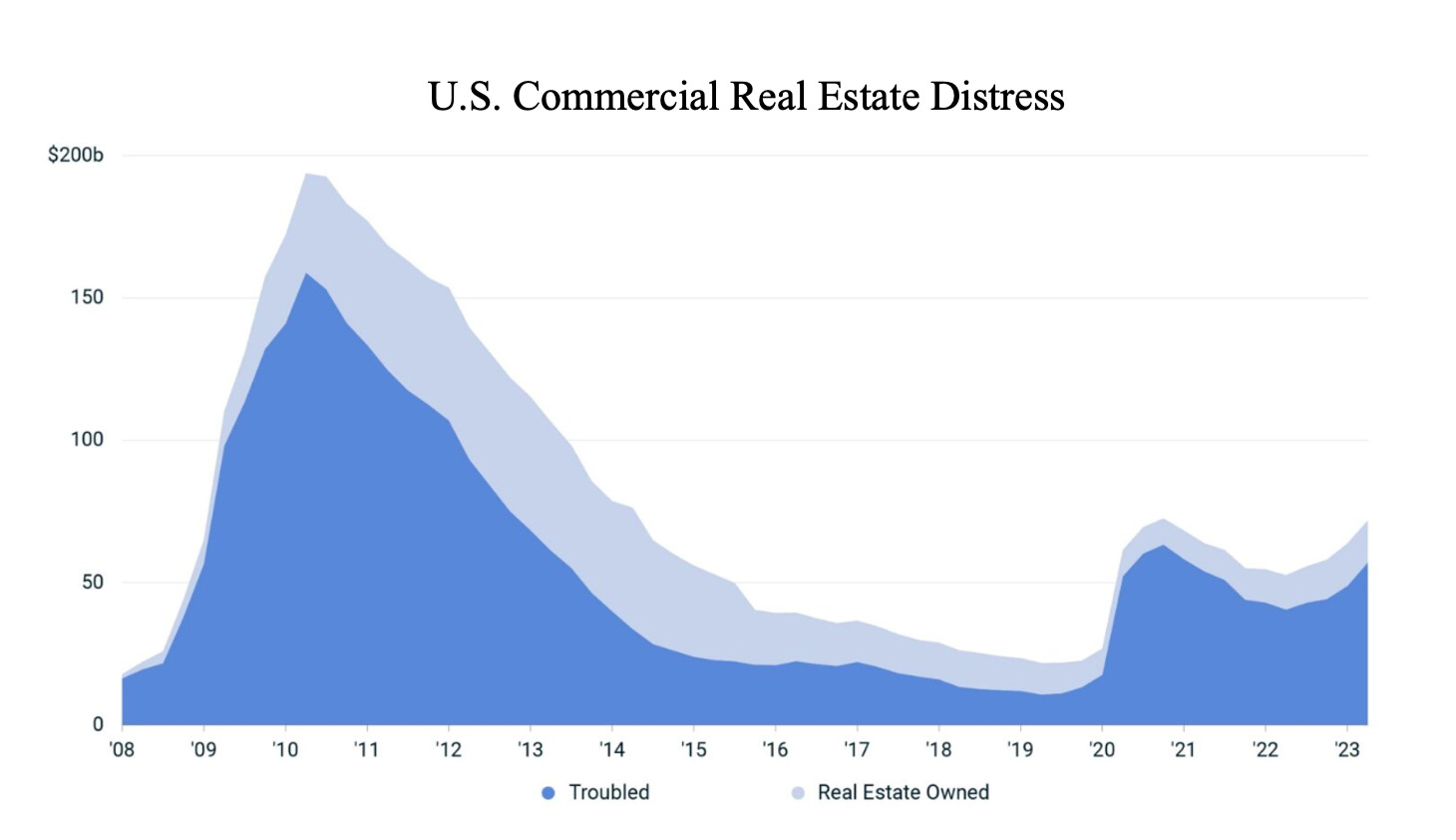

That someone is worried about rising CRE loan delinquencies isn't exactly newsworthy: CRE has been a slow-motion train wreck since 2020.

But when I saw that the FDIC, which isn’t exactly known for being ahead of the curve, was taking notice, so did I.

In a statement alongside its quarterly banking profile report for Q3 2023, FDIC Chairman Martin Gruenberg connected rising delinquencies in CRE loans with the risks posted by higher interest rates, suggesting that depositors should be concerned about unrealized losses of almost $700 billion across the banking sector.

When the Federal Reserve started hiking interest rates last year, low-yielding mortgage securities and loans lost value, chewing away at bank balance sheets. Tucked away in an accounting category known as “unrealized losses,” these phantom losses didn’t constitute a problem, until they did. We now know the story, when a flash bank run sparked in part by paper losses in its real estate loan portfolio, took down Silicon Valley Bank and ultimately led to First Republic's forced sale to JP Morgan Chase.

Despite the FDIC’s warning, Wall Street remains optimistic that the worst of the country's banking woes are behind us. The iShares regional bank ETF (NYSE: IAT), is at the highest level since the crisis earlier in the year, with the popular financial sector ETF (NYSE: XLF), within reach of its pre-crisis levels.

No doubt a nearly 100bps move in the 10-year yield over the past few weeks has helped buoy bank stocks, but the FDIC's warning is a fresh reminder that so long as interest rates remain elevated from a decade-plus of ZIRP (zero interest rate policy), bank balance sheets will remain under pressure.

This is one of several reasons for my view that the moment the Federal Reserve has cover to lower interest rates, they will. Banks - especially smaller and regional banks with a lot of bad commercial real estate debt - face worrying levels of paper losses that get a little less severe with every tick down in rates.

CHAT GPT TAKE

I asked ChatGPT to review the article and asses the implications for the US banking sector outlook:

Implications for the US Banking Sector Outlook:

· Risk Management Focus: Banks may need to strengthen their risk management strategies, particularly for CRE loan portfolios.

· Regulatory Scrutiny: Increased regulatory attention is likely, especially in areas like credit quality and liquidity.

· Financial Performance Concerns: The trend of declining net income and the increasing cost of deposits may impact the overall financial performance of banks.

· Market Volatility and Economic Uncertainty: The banking sector must navigate the challenges posed by economic uncertainties, including inflation and geopolitical tensions, which could affect loan and deposit dynamics.

· Asset Quality Monitoring: There will be an emphasis on monitoring asset quality, especially in light of the rising noncurrent loan rates in certain sectors like CRE.

Overall, the FDIC's report suggests a period of heightened vigilance and potential challenges for the U.S. banking sector, with a need for strategic adaptation to changing economic and market conditions.

Where to Invest in Commercial Real Estate? That Was the Question - Commercial Real Estate Observer

MY TAKE

Real estate conferences are not known as a source for novel investment theories, and the recent Capital Markets and Opportunistic Strategies Forum held by the Commercial Real Estate Observer was no different.

In its own summary, we heard such bold takes from industry experts as:

"You have to be in the market." (head of commercial real estate strategies at Amherst)

"We are in a distressed market." (managing director at Fortress Investment Group

And one chief economist took the leap of "taking Federal Reserve Chairman Jerome Powell at his word."

There was however, a nugget which caught my eye and confirms something that I keep hearing from the people closest to actual trenches of property distress.

Robert Dickey, managing director at Invesco, traced through how banking regulators and lenders are applying lessons learned in previous crises (S&L in the late 1980s/early 1990s, GFC in 2008-2010) to current market conditions.

To paraphrase, Congress gave a handful of well-connected and/or savvy firms and individuals a windfall investment opportunity via the Resolution Trust Corporation, which hastily disposed of distressed assets in the early '90s. The Feds then corrected their mistake after the GFC by raking a piece of investor profits earned on assets

bought through TARP, the Troubled Asset Relief Program.

Banks however, caught unprepared by the unprecedented collapse in residential home values nationwide, destroyed billions of dollars in asset value by jamming loans through foreclosure and fire selling assets into a declining market.

Dickey points out that this time around, lenders are wisening up. The special servicer industry for commercial mortgage backed securities "realized that 'extend and pretend' is now the best method to recover original loan balances.” Regulators are behind the scenes reminding bankers what happened last time they were a bit too trigger happy turning delinquent loans into REO (real estate owned).

Nevertheless, eager vulture investors are raising gobs of capital to jump on “distressed opportunities,” underestimating how aligned banks and their regulators are in avoiding another deluge of foreclosures. In truly distressed situations, lenders have realized that selling the note directly is a cleaner, quicker way to dispose of problematic assets, and not all these vulture funds have the chops to take down a loan and push it through to property ownership

Extend and pretend is a better option for lenders because outside the office sector, most properties with debt problems are otherwise operating just fine. Rents may be down, equity may be depleted or even negative, but the real problem is debt service at today’s rates. Banks are betting that if they can kick the can down the road a few months or years, they and the borrower could get bailed out when rates go back down (see comment above) and values recover.

CHAT GBT TAKE

I asked ChatGPT to read the article and assess where the best opportunities like for buying commercial real estate.

Assessment of Opportunities:

Hospitality Sector: Investment in hospitality, especially in resilient markets like New York City, is highlighted as a safe path, benefiting from regulations and sustained demand.

Off-Market Transactions: Due to the current market dynamics, there are unique off-market opportunities, particularly in scenarios where borrowers can transact directly with lenders.

Distressed Asset Management: In regions experiencing overbuilding or political risks, there are opportunities to acquire distressed assets and manage them for higher returns.

Regional Diversification: Shifting focus to states like Georgia, North Carolina, South Carolina, and Tennessee can offer better investment opportunities, avoiding the challenges present in markets like Florida and Texas.

Retail and Shopping Centers: Investing in malls and regional shopping centers could be beneficial in the long run, as these assets are currently undervalued with prospects for growth and increased leasing activities.

Overall, the best opportunities in CRE seem to lie in resilient sectors like hospitality, in exploring off-market deals, managing distressed assets effectively, diversifying into emerging regional markets, and focusing on long-term growth potential in retail and shopping centers.

San Francisco is Building to Bring Residents Back (paywall) - Wall Street Journal

MY TAKE

So I lied, you should not read this article unless you are looking for a good laugh.

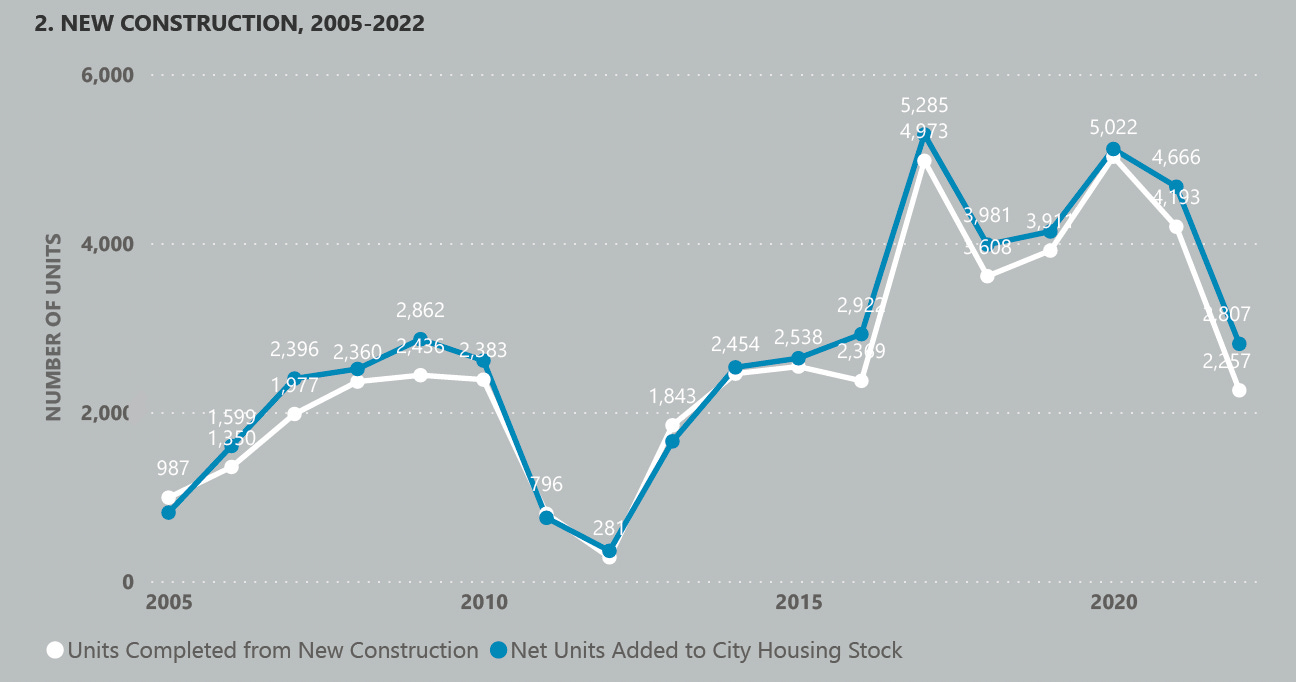

In defending the notion that “San Francisco is Building,” this Wall Street Journal piece cites a developer announcing plans for an outlandish downtown luxury project and a handful of office conversion applications that any insider will tell you is pandering to city leaders who are taking politically expedient half-measures that will have little impact on San Francisco’s housing shortage that grows worse by the day.

The facts are that through the first half of the year, the San Francisco Planning Department has approved fewer than 300 new housing units, and my analysis of SF Planning Department Data suggests that there are fewer than 2,000 market rate apartments under construction currently, or just over 1.0% of current inventory.

So no, San Francisco is not building. Construction activity is down sharply from last year, following the downward trend in the graph below.

The announcement of the planned development came from Los Angeles-based Bayhill Ventures, who envisions a 71-story, 684-unit luxury downtown high-rise with an expected completion date of 2028.

Reflecting the seriousness of this project, Bayhill founder Paul Paradis had the following to say about challenging conditions in the construction lending market: “We’re sort of avoiding that issue right now.” When asked about rents, Paradis suggests that Bayhill will charge “top of the market” rents of $8,000 per month for a 1,000sqft unit, which would be something like a 100% increase in market rents from today’s levels.

“We’re sort of avoiding that issue right now.” - Paul Paradis, Bayhill Development

Meanwhile, city officials are talking their book. Despite estimates that rents need to raise around 40% for new projects to make economic sense thanks in part to San Francisco having the world’s highest construction costs, Anne Taupier, development director of the city’s Office of Economic Workforce Development, suggests that “There is no better time to entitle a project than right now.”

Developers disagree, as entitled units in 2022 were the lowest in seven years, and as mentioned above, 2023 is set to come in far lower.

You have to at least give San Francisco credit for its public relations efforts.

CHAT GPT TAKE

I asked ChatGPT to read the article and assess whether San Francisco is really building to bring back residents.

“San Francisco's approach indicates a strong commitment to addressing its housing crisis and revitalizing the city's economic and residential appeal.

The initiatives reflect a strategic shift in addressing both the overabundance of office space and the need for more housing.

The developments, like the Bayhill tower, demonstrate confidence in the city's potential for a residential comeback, although they are also a sign of an evolving real estate market.

The reduction in regulatory barriers could expedite the development process, making the city more attractive to developers and investors.

However, the high costs associated with living in San Francisco, as exemplified by the projected rents for the new developments, suggest that attracting a diverse demographic might still be challenging.

The focus on market-rate housing over affordable units might raise concerns about inclusivity and the availability of housing options for all income levels.

Overall, San Francisco is actively building and adapting its policies to encourage residential growth and bring back residents. The success of these efforts will likely depend on the balance between market-rate and affordable housing, as well as the city's ability to maintain its appeal amidst changing economic and social landscapes.