Three Contrarian Commercial Real Estate Predictions for 2024: The Consensus is Wrong on Rates

Don't be afraid to bet against the crowd

The consensus isn't always wrong, but it usually is.

Every year big commercial real estate (CRE) brokerage houses, economists and pundits put out their version of the industry groupthink for next year's outlook for the industry.

So rather than toeing the line, here are three consensus-busting contrarian takes for 2024:

1) THE CONSENSUS IS WRONG ON RATES

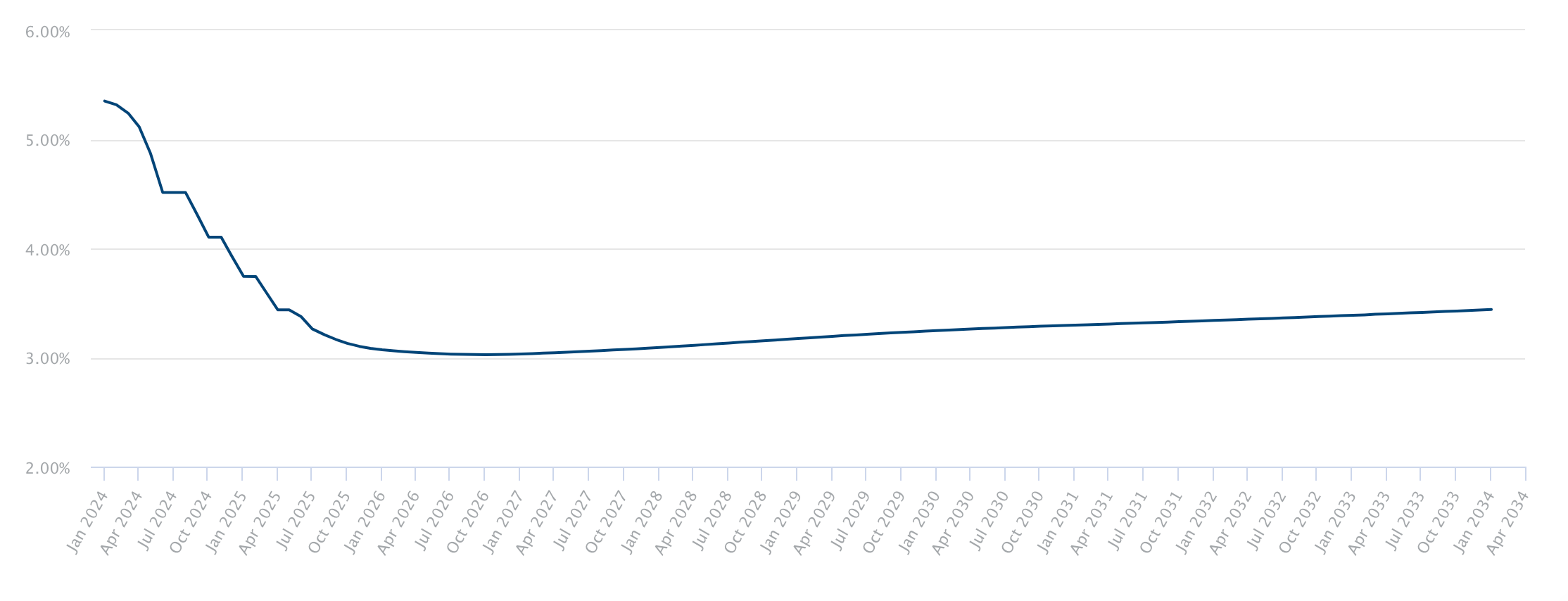

The entirety of the real estate complex is sure of a single fact: interest rates are headed lower in 2024.

But what if they're not?

The forward SOFR curve is pricing in almost 100bps of easing by June of next year, despite public dissent within the Federal Reserve over the future of rates.

Lower rates have obvious benefits for holders and buyers of CRE, in particular since it was the sudden rise in rates starting in 2022 that sent values skidding and borrowers into distress. So it's no wonder that the industry is reading through Federal Reserve Chairman Jerome Powell's cautious words and predicting lower rates starting as early as Q1 of 2024.

The premise is that with inflation in check (is it though?) and the U.S. economy headed for the elusive soft landing (is it though?), the Fed has plenty of cover to ease monetary policy to keep the economy humming without risking stoking the flames of inflation again (does it though?).

There are two primary risks to this goldilocks take, both of which challenge the view that lower rates in 2024 are a matter of when, not if.

First, geopolitical instability in the Middle East risks a commodity shock not unlike the one we saw at the outset of the Russia-Ukraine war. With shipping traffic being rerouted as Iranian-backed militias fire on private vessels in the Red Sea, escalation in the Persian Gulf could crimp oil supplies and send prices higher. Crude is actually down around 10% since October 7th, although it has risen in the past couple weeks as traders digest the impact a widening of the Israel-Palestine conflict.

Significantly higher fuel prices would crimp the Fed's ability to send rates lower, lest they lose credibility in their fight against rising prices.

The second risk to the consensus take on rates is that the U.S. economy takes off in 2024. If the consumer can defy high debt loads, digest persistently high food prices, and recycle money saved on easing rental costs, the much-awaited soft landing could end up being the pessimistic take.

Rapid growth is a tough environment for the Fed to be easing (although they've done it before, as recently as 2021-2022), and with market expectations so squarely in the lower, sooner camp, even this favorable economic outcome would likely be met with negativity in the CRE space.

2) OFFICE DEMAND COMES ROARING BACK

The only thing the CRE industry is more sure about than lower rates in 2024 is that the office market is years, if not decades away from recovering.

But what is the premise underlying that assumption is wrong?

We are already seeing cracks in the notion that hybrid work is a viable option for corporate America. Big tech companies, banks and even the federal government are pushing for workers to come back to the office.

Many employees love the flexibility of only having to come to the office a few days a week, but that is a luxury that workers can push for in a tight labor market. As companies continue to focus on the bottom line and research mounts that most workers are more productive in the office, employees lose their leverage.

The office property sector in the U.S. has been understandably decimated since the pandemic, with the nationwide vacancy rate now as high as it was during the Savings and Loan crisis of the late 1980s and early 1990s.

Most predictions of a recovery are measured in decades rather than years.

But those forecasts are based on the premise that hybrid work sticks and it takes years of organic demand growth to chew through existing vacancy.

If that underlying assumption changes materially, namely that companies can start demanding even four days a week in the office compared to the three that is becoming customary, the office recovery timeline shrinks dramatically.

With office properties in hard-hit markets like San Francisco and Baltimore trading at as much as 80% of their previous values, a shortened recovery timeline would handsomely reward bold investors buying now.

3) UNIVERSITIES FIRE SALE ASSETS TO RAISE FUNDS

The business of higher education has been under pressure in recent years, with College closures on the rise, driven by declining enrollment and a reliance on tuition income which struggles to cover bloated cost structures.

And the recent high-profile controversies at Harvard, MIT and Penn highlight the risks that these massive, tax-exempt institutions could see one of their primary funding sources dry up. For those that can fundraise from a wealthy donor base, Universities rely on huge endowments to fund investment and expansion.

But what happens is donors close their wallets or colleges can’t keep the lights on?

The 155-acre campus of Green Mountain College went up for auction in 2020.

In 2021, Forbes ran the headline: Colleges Short of Cash? Sell the Campus.

Earlier this year, Los Angeles-based BH Properties picked up the Holy Names campus in Oakland, California, with plans to repurpose the property but maintain its education use.

And this summer, Unity Environmental University put its 255-acre Unity College campus up for sale.

A quick Google search for “college campus for sale” returns a long list of other options should one want to own a little piece of the crumbling American higher education system.

This is not to suggest of course that Harvard is in any danger of going out of business, or that Stanford should consider selling off what was estimated in 2019 to be a nearly $20 billion real estate portfolio. But as colleges come under further pressure, expect the acquisition and repositioning of campus properties to become an important niche within the market for opportunistic property investments.